ICO Rankings Blog

Discover a wealth of knowledge and stay up-to-date with the latest trends, news, and insights in the cryptocurrency and blockchain space through our blog.

.png)

Discover a wealth of knowledge and stay up-to-date with the latest trends, news, and insights in the cryptocurrency and blockchain space through our blog.

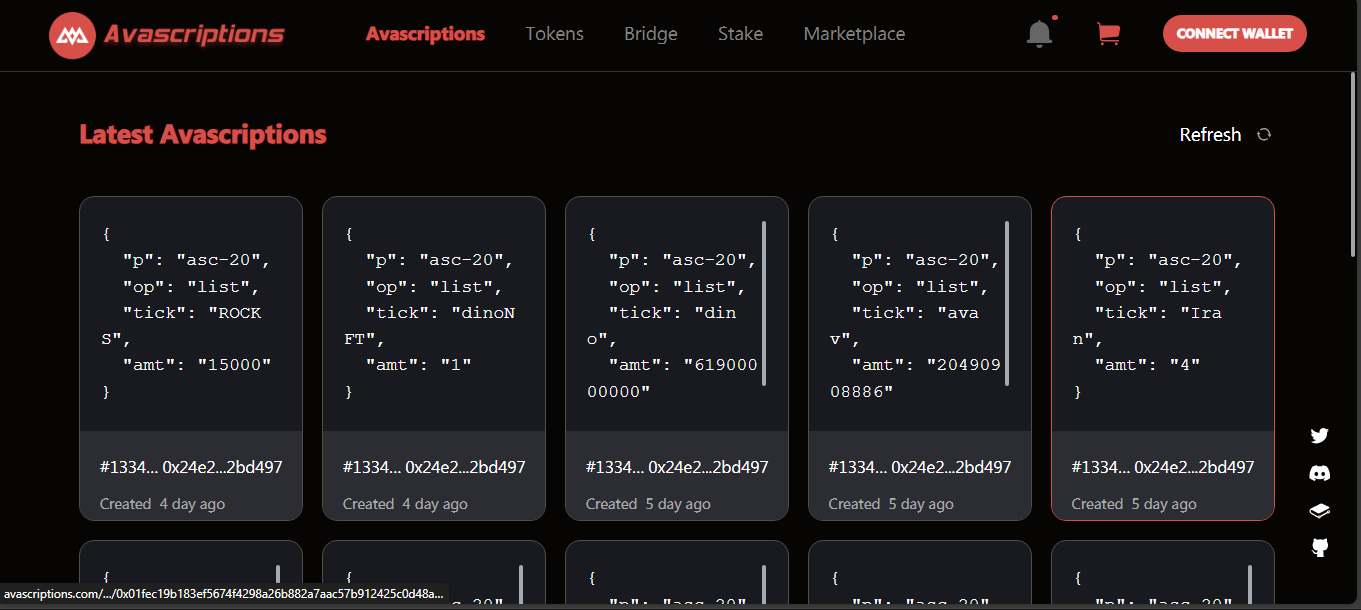

Avascriptions appears to be a crypto exchange project tied to its native token AVAV. It carries a name and a web presence, but beyond that it delivers almost no verifiable activity or history.

The exchange is conceptually linked to its own token, AVAV, which reportedly supports staking. Basic information suggests the project markets itself as a gateway for ASC20 token inscription and trading, hinting at token creation, staking, and crypto swaps.

On the data side, platforms widely report zero actual trading:

Although inactive, the project touts some concepts:

Everything outside the concept raises red flags:

Avascriptions looks like an undeveloped or abandoned crypto concept rather than a functioning exchange. There is no real liquidity, no user base, and no measurable activity. Even if staking exists, the lack of a visible trading venue or operational infrastructure makes it highly speculative and risky at best.

Avoid engaging with Avascriptions until tangible marketplace activity, verified audits, and user experience evidence appear.

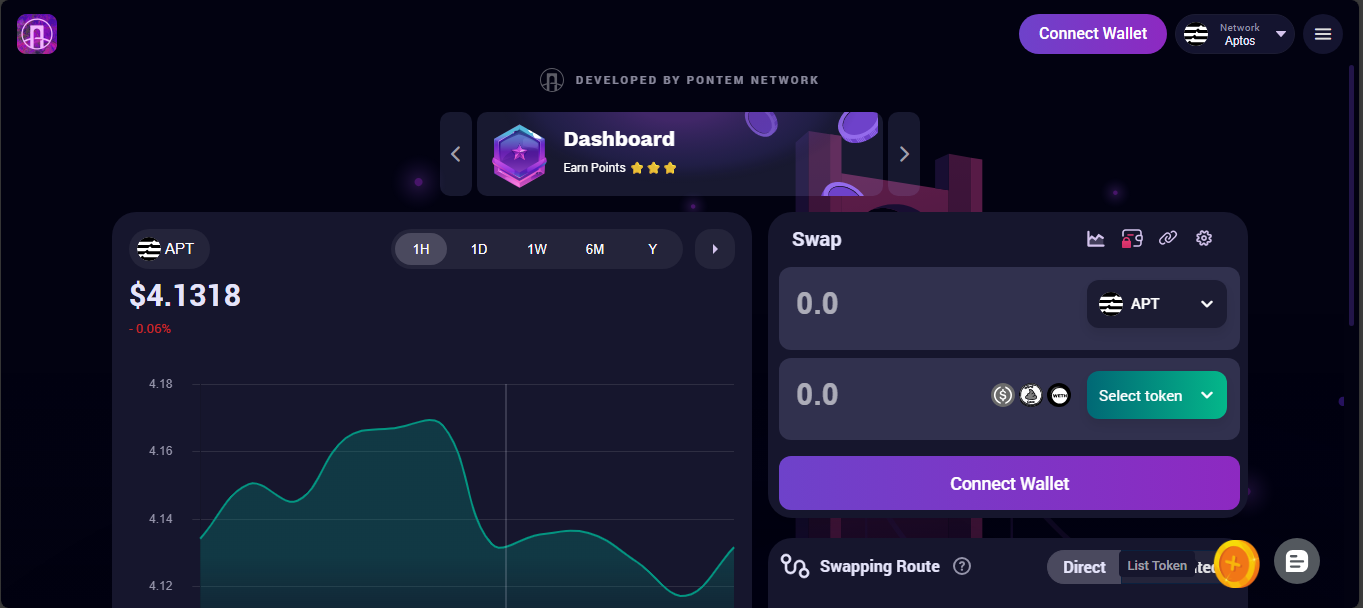

Liquidswap was created to be the main DeFi tool for Aptos. It is an automated market maker, where users can swap tokens, add liquidity, or farm rewards. At first, the project gained attention. It looked like something new for this young ecosystem. Over time, interest faded, and volumes went down.

The exchange supports two types of pools. One works for volatile tokens, another is for stable assets. Users can trade, stake their coins, or provide liquidity to earn a share of the fees. There is also a function to launch your own token. The interface is simple and works smoothly, even for beginners.

Security was part of the plan from day one. Liquidswap went through several audits, and the team added formal code checks. This gives it a level of trust that many new DEXs do not have.

Current numbers tell another story. The daily trading volume is very low, far below other decentralized exchanges. Only a few trading pairs are active, and liquidity is thin. In the past, total value locked was close to twelve million dollars. Now that figure is much smaller, and activity on the platform is quiet.

Despite its struggles, the project has some clear advantages:

There are also points that keep traders away:

Liquidswap started as a promising platform for Aptos users. It has strong tech, good audits, and features that work. But without traders and liquidity, it stays small. The potential is there, yet it is waiting for the market to catch up. For now, it is more of a niche tool than a leader in DeFi.

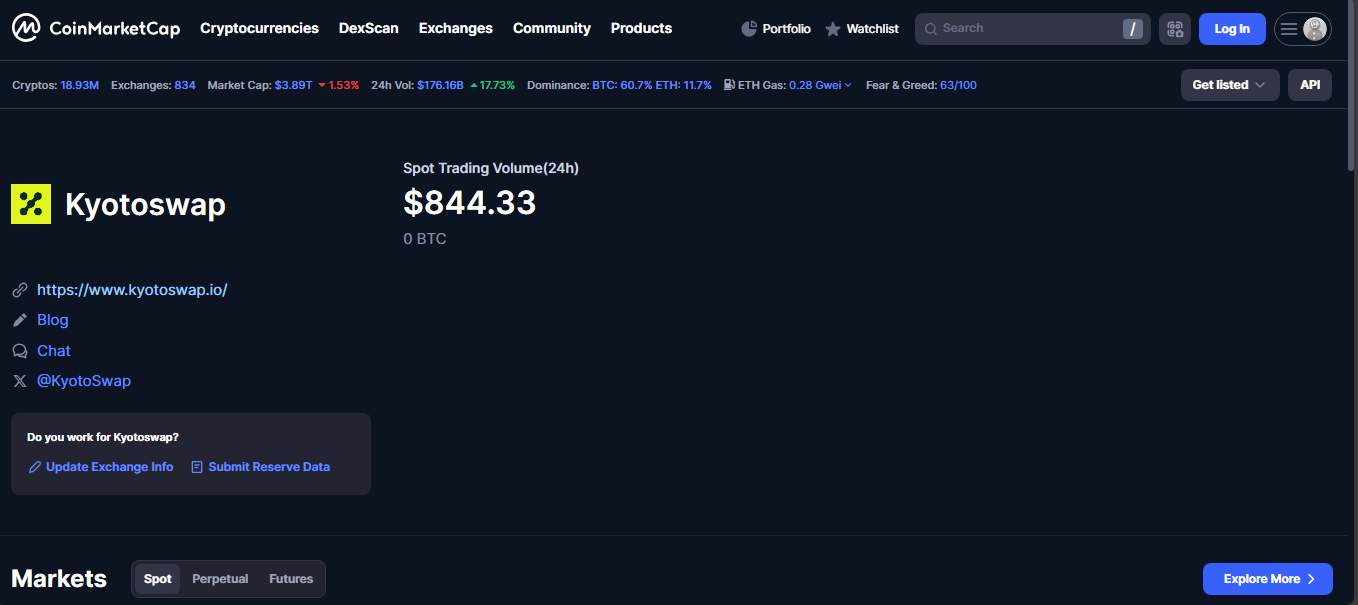

KyotoSwap claims to be a sustainable DEX where DeFi meets positive impact. It launched with a mission to offer eco-friendly swaps and community-driven growth. The idea was to combine decentralized trading with values, but the actual picture looks far less impressive.

The platform runs on the Binance Smart Chain with its native token KSWAP. It presented itself as a low-barrier exchange for users who wanted both trading and participation in socially responsible initiatives. Simple, transparent, and mission-driven - at least on paper.

Current data reveals very limited activity.

These numbers indicate that liquidity is far too low to support active trading.

Despite weak performance, KyotoSwap has some appealing elements:

The downsides are hard to ignore:

KyotoSwap started with an interesting idea, but in practice it remains barely active. The sustainability angle is unique, yet without liquidity, users, or a functioning market, it fails to compete with other DEXs. For now, it is more of a small experiment than a reliable trading platform.

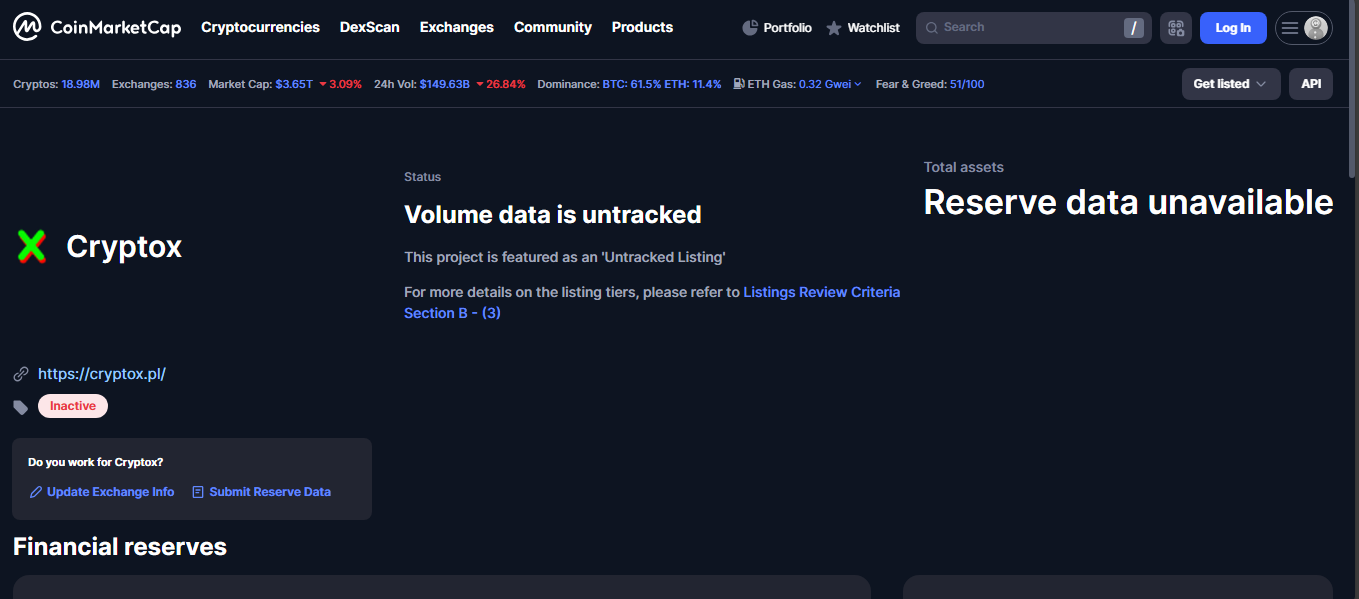

Cryptox back in 2016 or maybe 2017. It wasn’t a big deal, just one of those places where you could dump some coins or grab a quick trade. The signup was nothing – email, password, done. No ID, no stupid forms.

There weren’t many pairs. All trades went through Bitcoin. The site looked basic, almost boring, but it worked. Withdrawals were quick. Dash InstantSend made them faster than most places at the time.

Fees were almost a joke. Makers sometimes got paid for adding orders. Takers paid a bit, but not much. For small traders, it was fine.

Some folks liked it. They said trades were smooth, no problems. Others didn’t trust it – the team was a mystery, no audits, no info. But back then, nobody cared too much about that stuff if the site worked.

Then the market changed. Big exchanges came in with better tools, better everything. Cryptox stayed stuck in the past. Liquidity dried up. Orders just sat there. Nobody traded anymore.

Toward the end, a few users complained about slow withdrawals. Not a huge scandal, just enough to scare off the rest. And then one day, the site was gone. No warning, no goodbye. Just dead.

Cryptox had a short life. It worked, then it didn’t. No drama, no headlines. It just faded out, like many other small exchanges from that time.

Now it’s gone. No trades, no site, nothing left to see. Another forgotten name in crypto’s long list of dead projects.

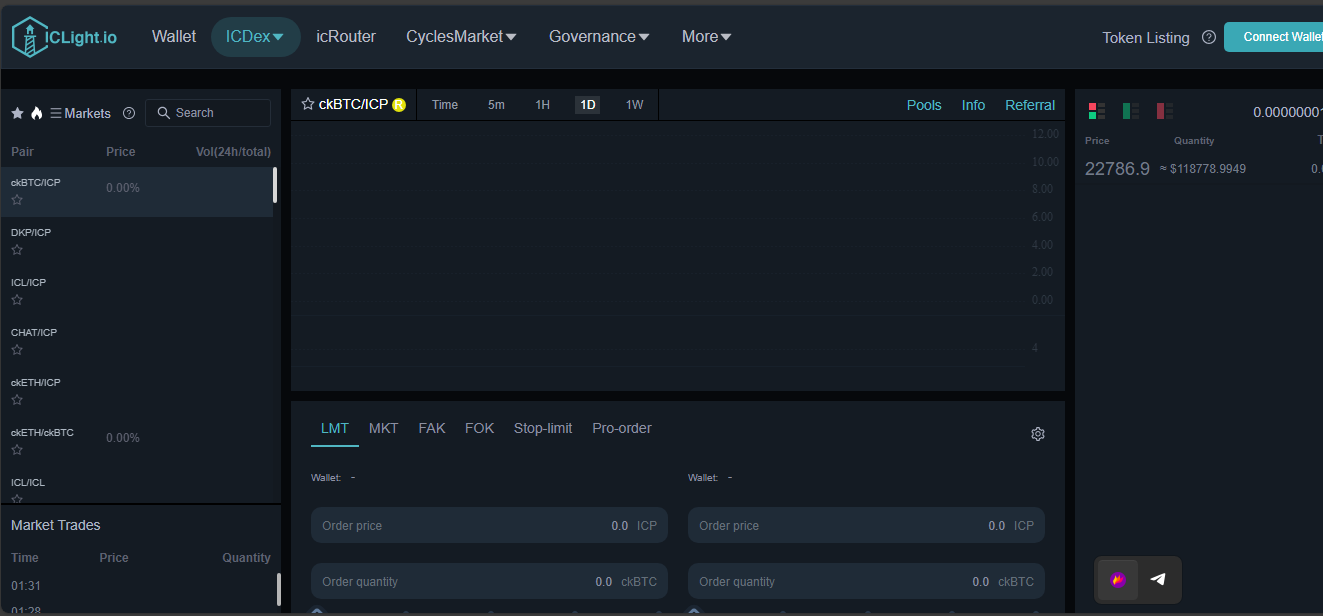

ICDex came out as a project that wanted to mix the feel of a centralized exchange with full decentralization. No custodial wallets, no middleman. Just an on-chain order book where trades settle directly on the network. It sounded fresh at launch. In practice, things turned out slower.

When you open ICDex, you see an order book and a trading screen that looks more like a CEX than a DEX. It supports limit orders, stop orders, even fill-or-kill types. Users keep control of their funds through smart contracts, which is nice. The number of listed tokens is tiny. Most trades focus on one or two pairs, usually related to ICP.

The daily volume stays very low, often around twenty thousand dollars or even less. Order books are thin. You place a larger order, and the price moves fast. Maker fees are zero, takers pay a small percentage, usually under half a percent. Still, with so little activity, even low fees can’t make up for the lack of liquidity.

The tech is solid. ICDex actually delivers a real on-chain order book with advanced order types. The code has gone through audits, and the design feels well thought out. For those who want to trade ICP tokens in a decentralized way, this is one of the few places to do it.

The problem is adoption. Almost no one uses it. There’s no strong community, no hype, and no signs of growth. The platform lists only a few coins. There’s no mobile app, no fiat access, no features that could bring in a wider audience. Without traders, an exchange doesn’t live up to its promise.

ICDex tries something different. It gives traders a proper order book on-chain, something rare in DeFi. The platform works, but almost nobody is there to use it. Without more tokens, more users, and better visibility, it stays a niche tool for a small group.

Right now, ICDex feels more like a test run than a real marketplace. It could grow one day, but at the moment it’s quiet, almost empty, and easy to miss.

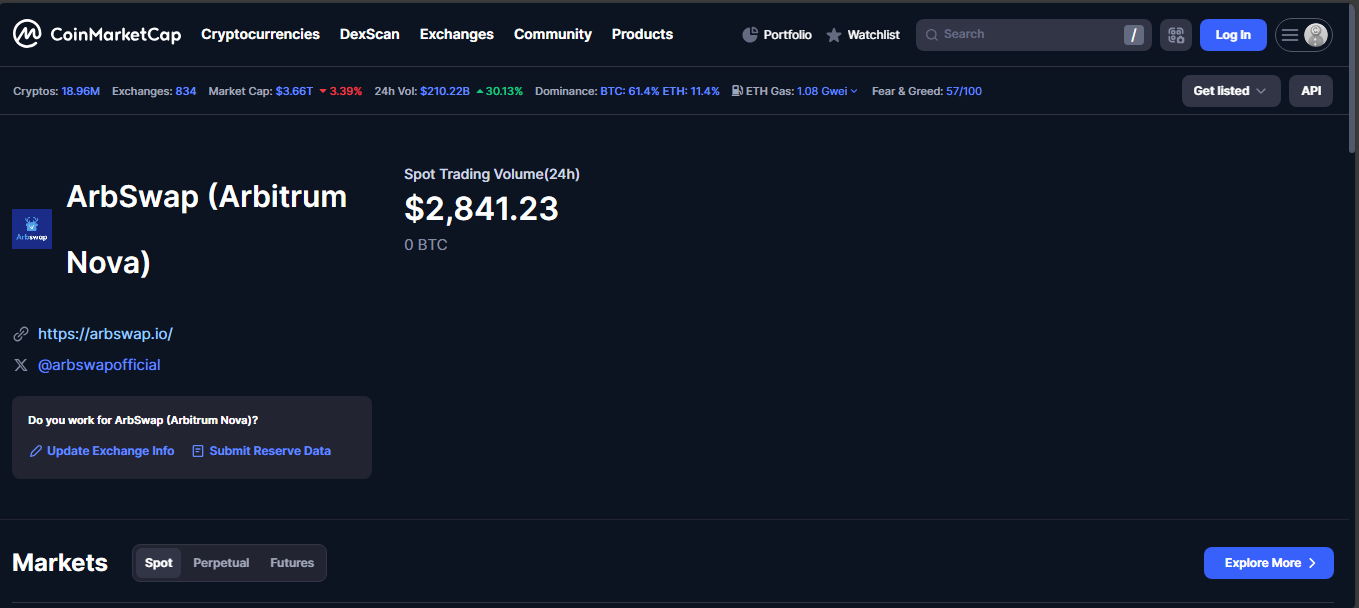

Arbswap launched in 2023, aiming to serve Game-Fi and NFT-related ecosystems on Arbitrum. The project promotes itself as the main DEX for in-game assets. The list of supported tokens is short, and real trading volume is almost non-existent.

The exchange is non-custodial, built specifically for Arbitrum users. It combines token swaps with bridging between Arbitrum One and Nova using LayerZero technology. Users can swap, bridge, and participate in yield farming, though all features remain tied to its small Game-Fi focus.

Reported daily trading volume rarely goes above five thousand dollars. Most activity happens on one pair, while the rest of the market stays empty. User feedback is almost absent, and no community growth is visible. Traffic to the site is extremely low, confirming that the exchange is barely used.

Arbswap tries to position itself as a niche DEX for Game-Fi assets and bridging on Arbitrum. Technically, it works, but real usage is almost zero. Liquidity is too thin, and without growth, it stays a risky choice. For now, it looks more like an experimental project than a functioning marketplace.