ICO Rankings Blog

Discover a wealth of knowledge and stay up-to-date with the latest trends, news, and insights in the cryptocurrency and blockchain space through our blog.

.png)

Discover a wealth of knowledge and stay up-to-date with the latest trends, news, and insights in the cryptocurrency and blockchain space through our blog.

Rippex popped up in Brazil as a niche exchange for Ripple (XRP) trading only. The fee model was simple - flat 0.30% per trade, same for maker and taker, and BTC withdrawal cost around 0.0009 BTC.

It never expanded. No other cryptos, no fiat options besides wire transfers, nothing exciting. A one-coin shop - fine maybe for fans of XRP, but limited and risky if demand dried up.

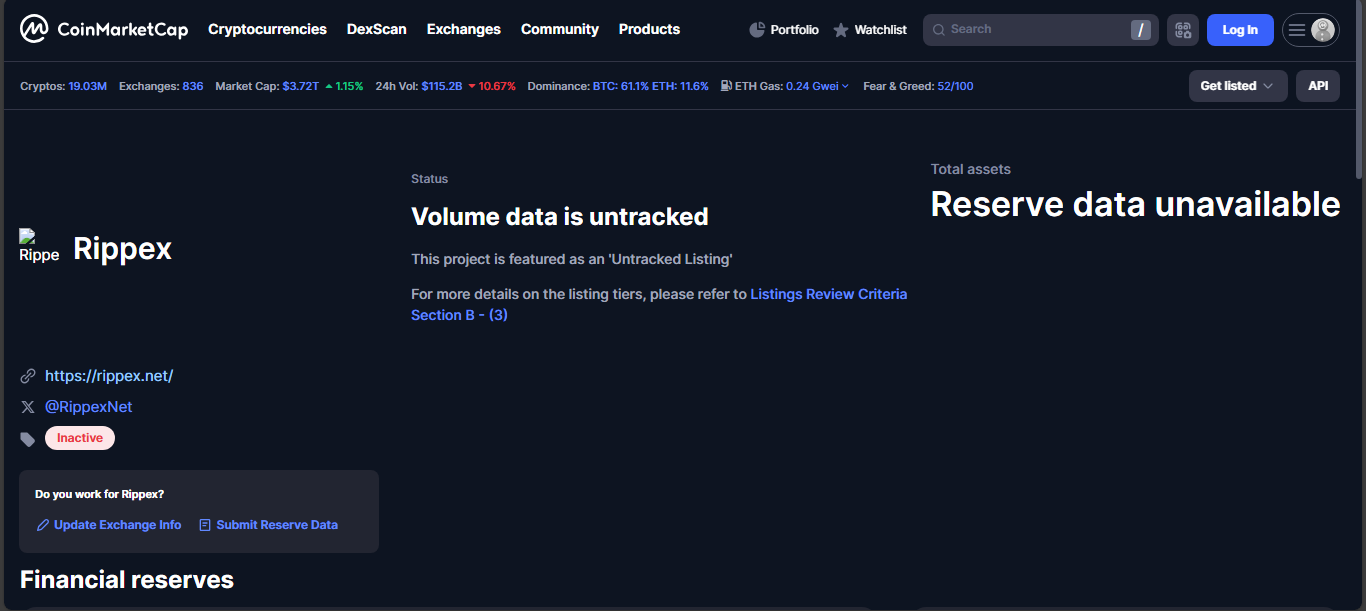

The platform was flagged inactive long ago. They stopped deposit and trading services, the website turned dormant, and eventual announcements were vague or missing. It became clear they shut down completely.

At the end, liquidity was nil. No one was trading. No visible activity. The site itself showed a notice (in Portuguese) saying the exchange was permanently closed. Users had no real path to reclaim funds once services halted.

Zero trading. Zero liquidity. Zero support. The company faded. It’s a name on old listings now - a reminder that single-asset exchanges with no reserves or backup plans vanish fast.

Rippex had a narrow bet - XRP only trading, flat fee structure, minimal features. That might have worked if it scaled, but it never did. Without expansion, liquidity, audits or broader support - it couldn’t survive.

Now it’s gone - no funds, no service, no comeback. A stark signal: when an exchange lacks variety, regulation, or resilience, a shutdown can come silent and final.

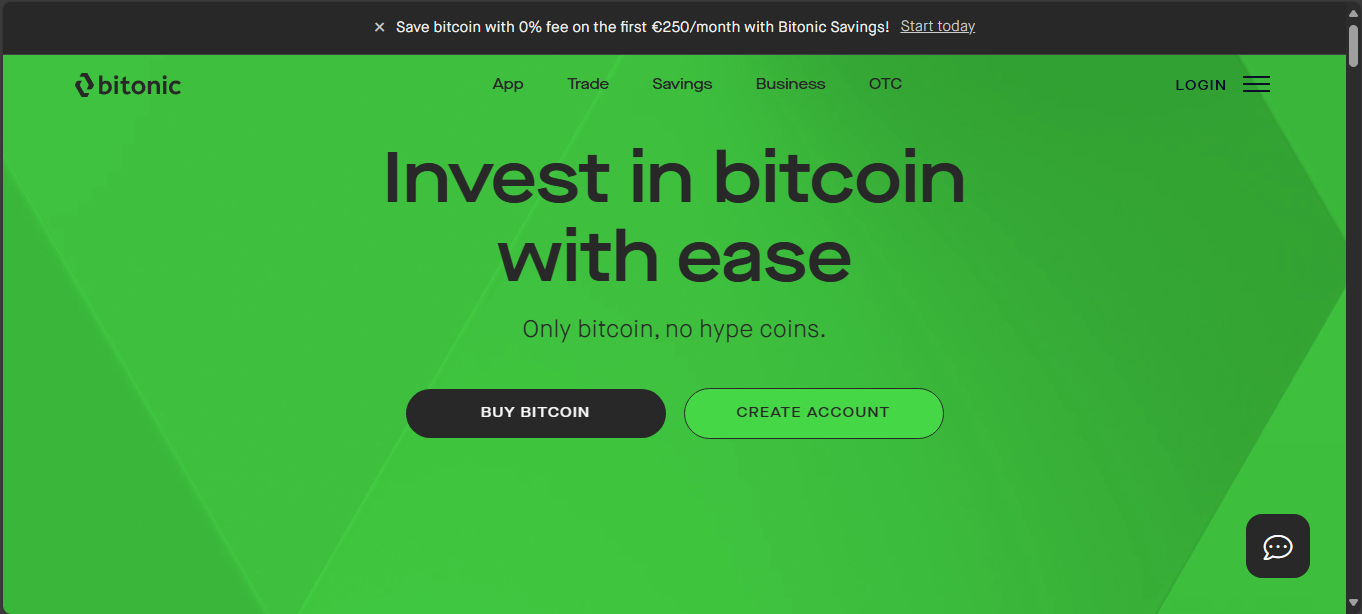

Bitonic started in Amsterdam with a simple idea - buy or sell Bitcoin with euros, nothing else. They kept it clean: fixed fees, easy deposits through iDEAL or SEPA, direct trades. For locals and beginners, that was enough. Over time they added a few extras like a savings plan and an OTC desk, but the core stayed the same.

Security was always part of their pitch. Cold storage, multi-sig, compliance with Dutch Central Bank. Reviews? Mixed. Many like the friendly support, some complain about slow KYC or endless document checks. It’s a regulated service, so the process can be heavy.

Only BTC trading. No altcoins, no token farming. You buy with euros or sell back. Fees sit around 0.25–0.60% per trade, depending on order type. You can set up recurring buys, and withdrawals in fiat are cheap or free. The interface is simple enough for anyone to use.

It’s clear and stable, but also limited. One coin, one market. Great for small trades, not built for big ones.

Liquidity isn’t strong. Daily volume is low, so large orders may slip. Transparency on reserves isn’t visible. Some users point to delays during verification and price differences during busy times. For a small platform, these things matter.

In 2025, Bitonic is still alive. They trade BTC/EUR, offer savings, answer emails, even phone calls. Their app works fine. But they never grew beyond that tight focus. No altcoins, no expansion, no major updates.

Bitonic never tried to be everything. It stayed local, stayed small, and stuck to Bitcoin. That makes it simple and, for the most part, safe if you’re in Europe and just need to buy or sell BTC without hassle.

But if you’re after altcoins, heavy trading, or deep liquidity, it won’t cut it. Bitonic is fine for what it is - a quiet, narrow exchange that never chased growth.

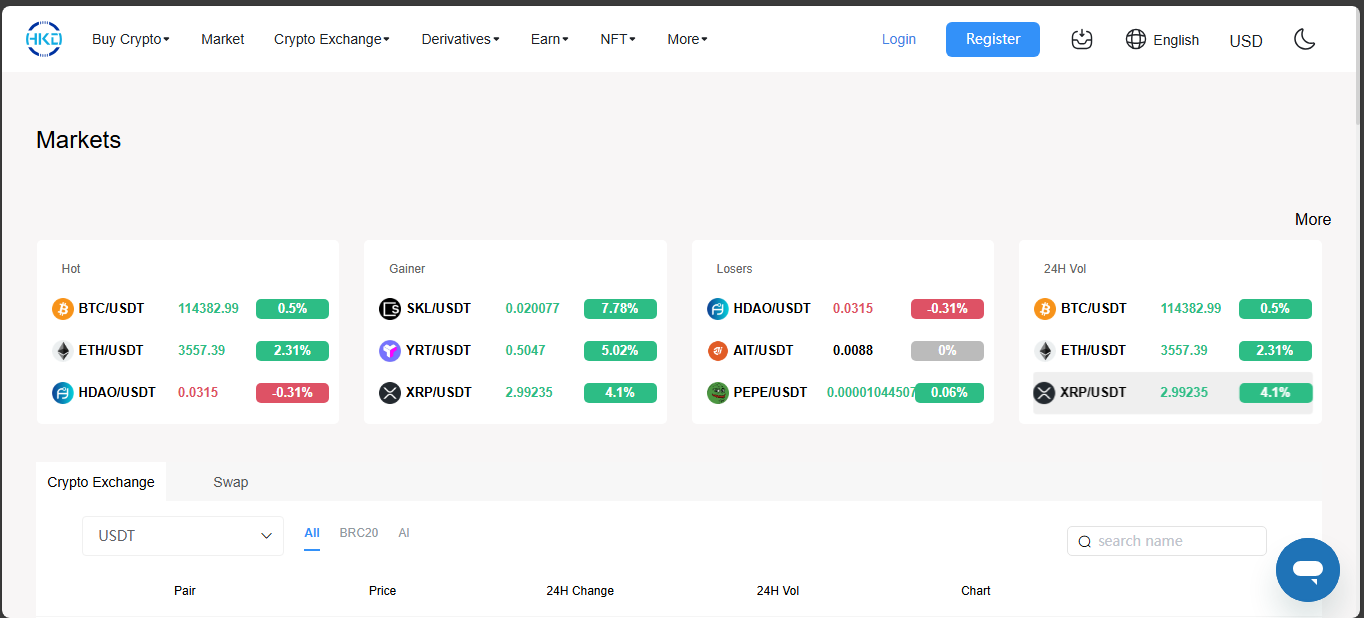

HKD.com showed up in 2019, pitched itself as a global-friendly exchange with spot, perpetual and futures markets. It handles over $1 billion in daily volume - think thousands of BTC traded in 24 hours. It supports around 23 crypto assets and claims liquidity for pairs like BTC/USDT, ETH/USDT, XRP/USDT, SOL/USDT. But reserve proof? Unknown. Transparency? Missing.

Traffic numbers? Low single-digit thousands per month - suggesting much of the volume comes from bots or institutional connections. User reviews are nearly nonexistent, and the overall trust score feels flimsy.

You get spot, perpetual and futures trading support with moderate selection - under 25 coins. Fees are advertised as low, but public documentation is thin on details. Fiat support? None. KYC? Yes, mandatory. Withdrawals operate in crypto only. Site claims global service but mostly handles USDT and other stable pairs.

Volume may seem attractive - but without reserves data, it’s hard to trust. Liquidity varies depending on pair. The interface is functional but not polished - some reviewers cite app issues and geo-limited language support.

Proof of reserves missing. No audit certificates. Community feedback almost zero. Domain traffic under 6K visits a month. That level of opacity undermines confidence.

HKD.com still runs markets - BTC, ETH, XRP, SOL, etc. - volume hovers near $1 billion per day. But user activity appears minimal. No independent verification of liquidity claims. No clear growth or expansion, and the user base remains unclear.

HKD.com is odd. On one hand it handles big numbers. On the other, it hides most of the operational details. If that volume is real, then the platform may serve a niche of bots or institutional flows - but retail users get no visibility into reserves or audits.

For traders who need proof and clarity, it’s shaky ground. The numbers might impress, but when you dig deeper - transparency is missing. HKD.com works, maybe. But it doesn’t invite trust.

IOTA Exchange once appeared as a spot or perpetual platform linked to the IOTA ecosystem. On paper it offered trading pairs, maybe derivatives or token swaps - but none of that ever showed real usage. As of now, CoinMarketCap labels it untracked, and all the usual metrics - volume, liquidity, reserve proof - are completely absent.

There’s zero public data. Markets show no listings. Reserve fields are empty. No order books, no trades, no updates. It's as if the platform quietly shut down before anyone really noticed.

No audit info, no governance snapshots, no community feedback. The exchange doesn't appear in active aggregator feeds. Domain or ownership details are missing. It operates in total obscurity.

Still inactive. No trading, no deposits, no visible user base. Essentially, a ghost listing with no substance behind it - even though the name lives on in old directories.

It serves as a reminder: platforms that lack transparency and never attract volume may simply vanish. IOTA Exchange may have existed in concept - but without execution, it faded before becoming credible.

IOTA Exchange looked like a nice fit for the IOTA ecosystem - a tailor-made trading platform, perhaps. But if there was ever trading, it didn’t last. Now, years later, nothing remains: no volume, no transparency, no platform. It’s a textbook case of what happens when a project never gains traction and slips into oblivion.

ErisX came out, it had the image of a safe bet. Fully licensed, working under U.S. regulations, offering spot markets and physically settled futures. Traders were supposed to trust it. Institutions too. But the buzz never turned into real activity.

Cboe stepped in, bought the platform in 2022, and folded it into their digital plans. It sounded like the start of something big. New partners joined, new features were promised. Yet the market stayed cold. No volume, no crowd, no growth.

By 2024, Cboe decided to close the spot side. Futures didn’t die - they were moved under Cboe’s bigger derivatives arm. The change was quiet. No scandal, no hacks. Just a slow end to something that couldn’t hold on.

In 2025, ErisX as an exchange is gone. You won’t find public order books or traders using it. The name still pops up, but only as part of Cboe’s history. It faded out, simple as that.

The structure was there. Licenses, solid backers, a product mix that looked fine. But crypto needs more than that. It needs people trading, liquidity, movement. ErisX never had enough of it.

ErisX had everything on paper, but crypto doesn’t run on paper. It runs on users and trust. Without them, even the most compliant exchange fades. By 2025, ErisX is just a name people mention when they talk about what could have been.

Eqonex launched in 2020 from Singapore under Diginex’s umbrella. They marketed a full crypto exchange, spot trading, derivatives, token EQO with staking and fee discounts. Liquidity and volume spiked in 2021 - April alone hit over $1 billion monthly, thanks to institutional liquidity partners and EQO token launch.

Still, skepticism followed. Some reports questioned whether that volume was artificially inflated or inconsistent with real market activity. Users poked at missing transparency - no public reserves, minimal audit data.

On August 22, 2022, Diginex announced it would close the exchange. Users had until September 14 to withdraw funds. The move was strategic: pivot into asset management and custody services like Digivault instead of loss-making exchange operations.

By November 2022 the platform declared bankruptcy. Cryptowisser marked it as dead, placing it firmly in their exchange graveyard.

As of 2025 the exchange is fully inactive. Perpetual and spot trading are delisted or frozen. Trading volume has vanished - even official trackers list zero activity and no pairs live. No transparency remains, no community buzz, no updates. It’s a name in a database now.

They had ambition: licensed, equity-listed, token rewards, institutional partners. But execution stumbled. Without genuine market activity and trusting users footing the bill, the platform didn’t scale. And in crypto, glory without traction is short-lived.

Eqonex had the setup: regulated, Nasdaq-listed, token incentives, liquidity partners. But crypto users moved on, volume dried up, and the platform never became self-sustaining. By 2025 the exchange is gone. Its story reminds us: even well-backed projects can vanish quietly if they fail to retain real user engagement and transparent infrastructure.